The high cost of Joe Biden’s America

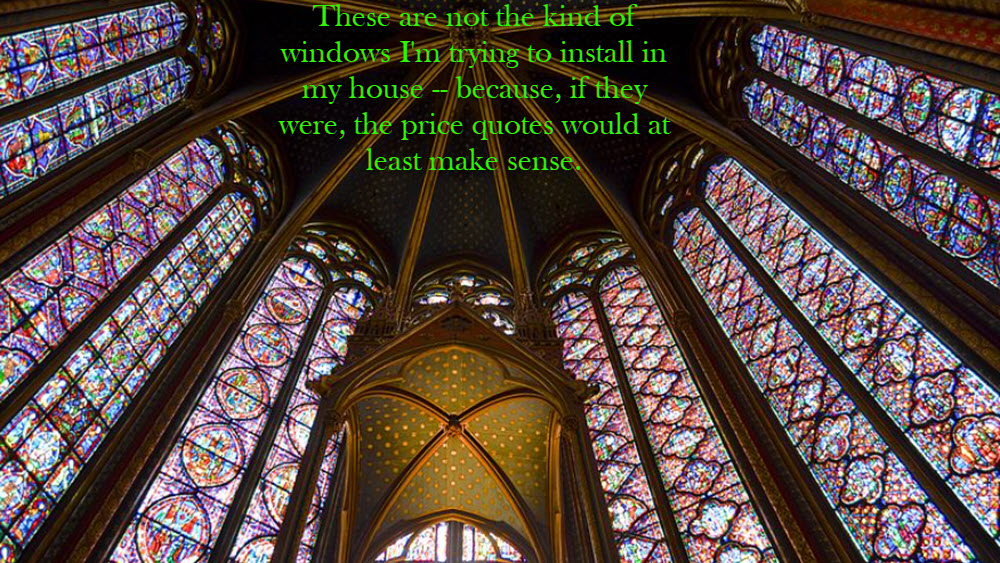

Replacing windows in the house is a snapshot of what Joe Biden has done to America.

Continue readingConservatives deal with facts and reach conclusions; liberals have conclusions and sell them as facts.

Replacing windows in the house is a snapshot of what Joe Biden has done to America.

Continue reading

So, I finally did it. When I organized the images (as I always do), I added a new category: New World Order. You’ll recognize it in the lineup when you see it. COVID update: To date, COVID has been like any other flu I’ve ever had. The problem with this

Continue reading

The news is hitting so hard and fast, and from so many different angles, that the only theme here is that I have lots and lots of memes.

Continue reading

With the Supreme Court whipping out decisions and Democrats still on a rampage, I’ve got too many memes to wait until Friday. A caveat goes with the next one: The Supreme Court was addressing a very specific law. However, the principles laid out mark the death knell of red flag

Continue reading

Even before the Supreme Court handed down its ruling, my collection of gun memes was big. I’ve got a few other great memes too — about 100 of ’em. Before I get to the memes, I may finally have resolved most of the problems that have been bedeviling me for almost a

Continue reading

It’s not really the end of the world; it just feels like that. And these memes will help you laugh and cry that feeling away.

Continue reading

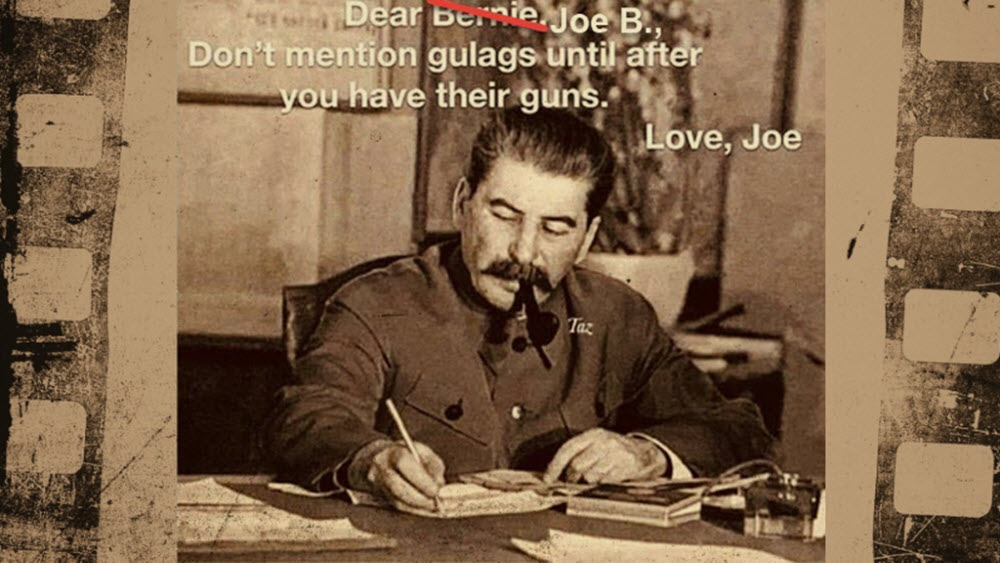

Once again, judging by the memes I got, while Dems are obsessed with January 6, real Americans care about guns and the aggressive LGBTQ+++ movement.

Continue reading

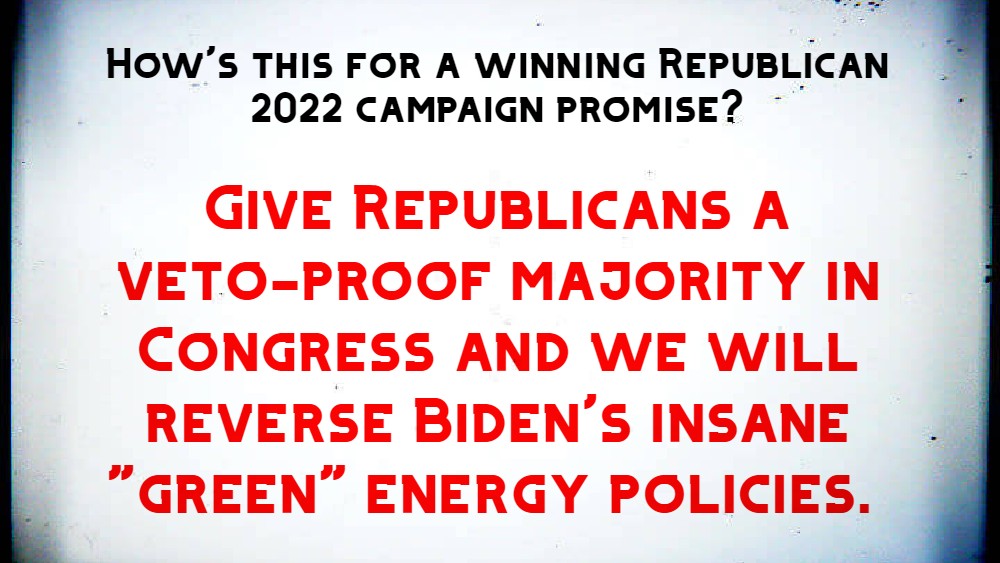

These memes are a reminder it’s not enough to re-take Congress. We need a veto-proof majority to undo some of the damage.

Continue reading

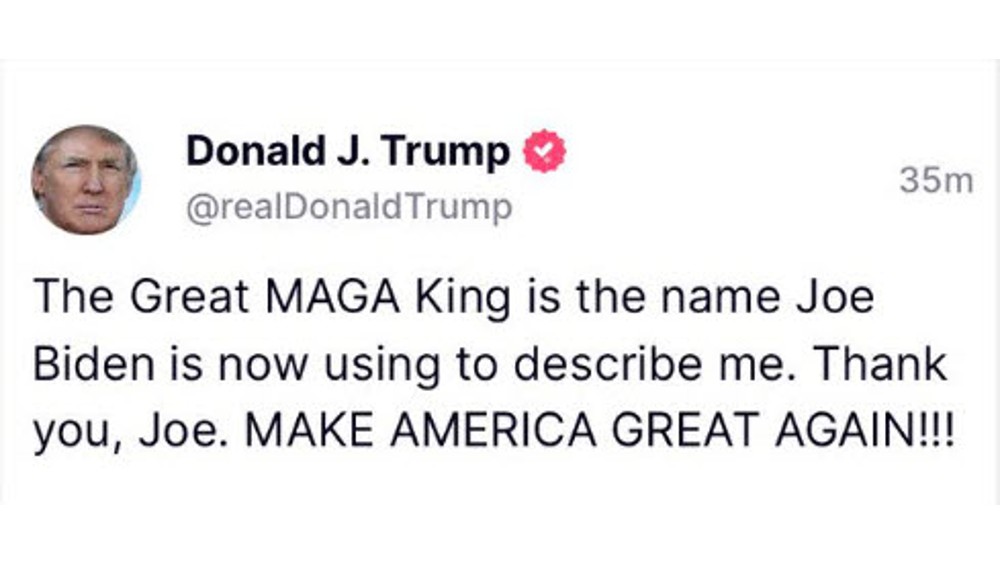

Trust Joe Biden to think really hard and, instead of insulting conservatives, come up with the best praise ever…plus other great memes. And the return of a classic: The Great Maga King!#TheGreatMagaKing pic.twitter.com/8zmwvaNrVq — Mad Liberals (@MadLiberals) May 12, 2022

Continue reading

The bad news is that Democrats are in power. The good news is that they are so awful, Americans are waking up. Plus, good memes. If you’ve lasted this far, I have some news. First, I think I finally got a tech person who made a difference. Loading this illustrated

Continue reading

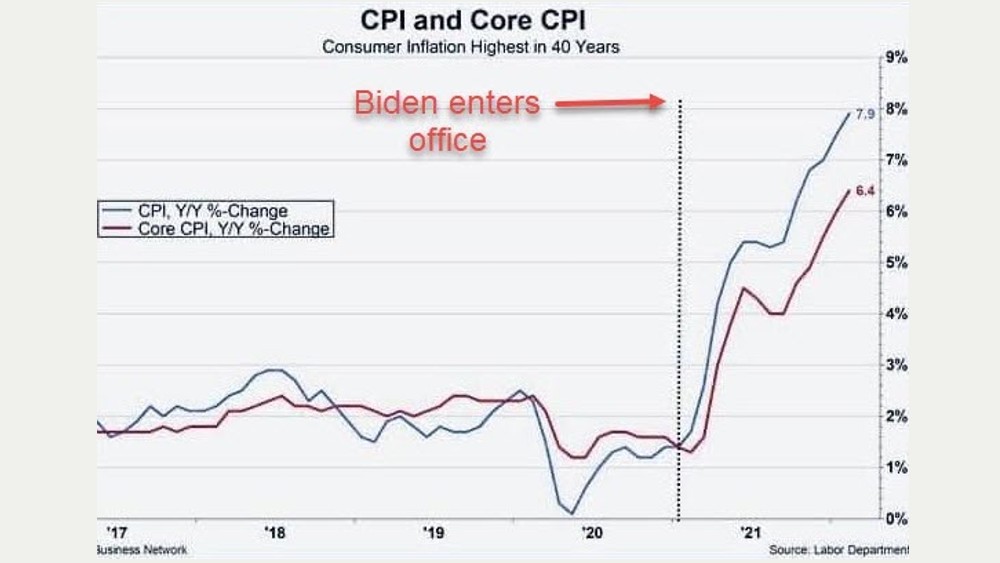

This should take your mind off taxes but, given how insane Biden’s America is, I doubt it will make you feel any better about things.

Continue reading

Bad times, as I always say, make for good memes — and I’ve got so many I can’t wait until Friday.

Continue reading

Is it possible…could it be…might it happen…. Here’s the question: Have the Democrats finally gone too far?

Continue reading

Actually, I don’t know whether we’re living in a computer simulation. I just know that, looking at these memes, it’s a very real possibility.

Continue reading

If this is where we are after 1 year of Biden, what will 3 years of Biden be like? I don’t even want to imagine. Let’s laugh while we still can.

Continue reading